It seems the two weeks of Brisbane winter have been and gone, which means we now start the countdown to summer.

With 20 weeks until Christmas (yes, it is that close!), it is a good time to take stock of what the year has brought so far – have you hit your business goals, your savings goals? If you find you haven’t quite gotten to where you want to be, there is still plenty of time to turn things around before 2017 is over.

If you run your own business, read our Roadmap to Business Success as a starting point to getting yourself back on track.

If you are investing, saving or generally trying to improve your personal financial situation, contact us for a copy of our Wealth Planner as the starting point to get you back on track.

Is It Sufficient To Have Life Insurance In Super?

(contribution by Mike Bendall from Era Wealth Management)

Life insurance can be held within your superannuation fund or via an external policy – or both.

What are the pros and cons of having your life insurance in your superannuation fund?

One option for many, when it comes to life insurance (as well as total and permanent disability/TPD insurance and income protection insurance), is to hold that insurance cover through their superannuation fund.

Statistics show that around 83% of superannuation members sign up for the default insurance cover, offered by their super fund. Is that a good idea?

Remember there are pros and cons with relying on your super for all your insurance needs. Sure, it may be cheaper, but often superannuation insurance cover is nowhere near as far-reaching as a stand-alone life insurance policy.

Often life cover in super is usually only for $100,000 or $200,000 when in reality you may need closer to $500,000 or $1 million-plus to protect your family.

Advantages of life insurance through super

There are a number of potential advantages to holding life insurance through your super fund, including the following.

- Life insurance through super is more manageable – the premiums are deducted from your superannuation account balance rather than out of your own bank account. It still costs you either way, but if you have a home loan and family to raise then having the premiums deducted from your super account may make it easier on your cashflow.

- There can be tax benefits to holding life insurance in super – you can arrange to salary sacrifice the cost of the premiums if you don’t want to reduce your superannuation balance. This can be very tax-effective for workers on at least the average income tax rate, and for those who are self-employed Note, though, that funds you salary sacrifice to superannuation can’t be withdrawn again until you meet a condition of release, so you are locking your money away

Disadvantages of insurance through superannuation Along with the advantages outlined above, there are also some potential disadvantages of holding life insurance through superannuation. These can include the following:

- The amount of life insurance cover may not be sufficient for your needs – check whether the fund allows you to apply for extra insurance cover, or consider a second life insurance policy, held outside superannuation.

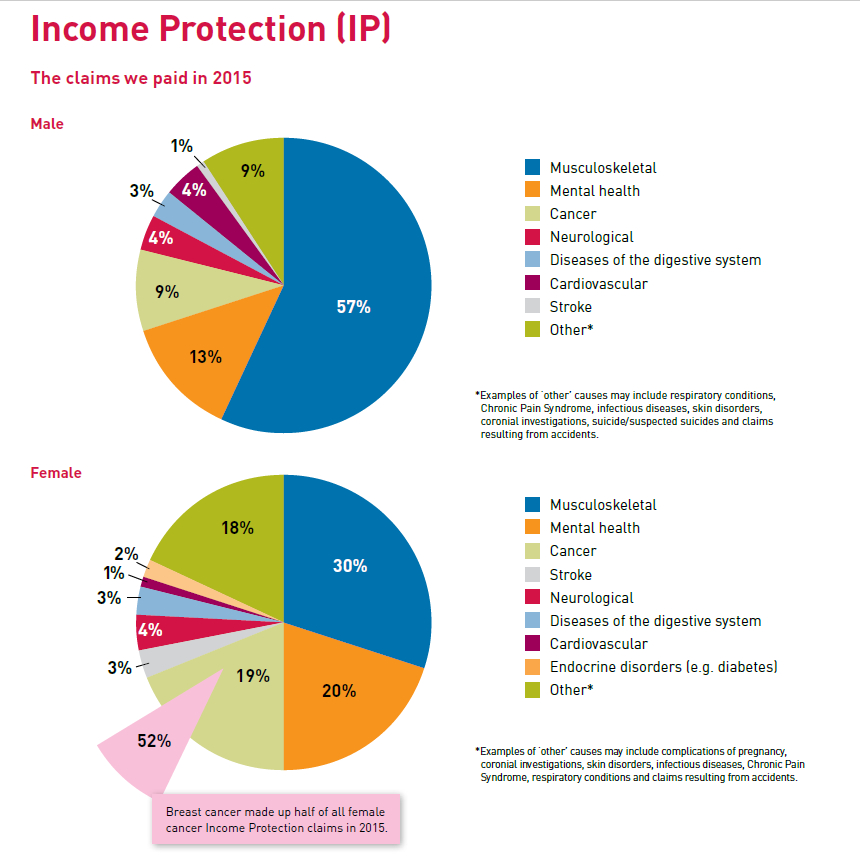

- The income protection benefits may be limited to covering only a certain percentage of your income for a short length of time. A second income protection policy, outside superannuation, may be needed to cover the shortfall.

- Trauma Insurance is not available through super funds – also known as trauma cover or critical illness insurance, trauma insurance provides a lump sum of money to cover immediate medical expenses and other financial needs when a critical illness or injury occurs. Having income protection insurance in place will cover a portion of your income if you cannot work due to illness/injury, however it doesn’t cover immediate medical and financial needs. Trauma insurance is a standard policy in standard life insurance policies outside of super funds.

- You may not be able to guarantee who the beneficiary will be – the decision as to the distribution of a superannuation death benefit often rests with the Trustee of the super fund. You may be able to make a binding death nomination, however you are limited in who can be nominated. If you need absolute certainty as to who will receive the death benefit, a super fund insurance cover may not be for you.

- The life insurance payout may be delayed – because the insurance payouts have to go to your superannuation fund before they go to you, and the Trustee then has to satisfy itself as to the correct beneficiary, there can sometime be a delay in the death benefit being paid out.

- There could be tax implications for death benefits – if death benefits are not paid to someone who was financially dependent on you, they may be taxed on the proceeds. You should seek advice from your accountant in relation to this.

- Income protection policies don’t last for too long – most income protection policies inside super provide for only two years’ worth of income protection – what if you cannot work for several years longer than that?

At the end of the day there is no right or wrong answer when deciding whether or not to have life insurance cover in your super fund. However, it is important that we understand the impacts on our insurance relative to our circumstances, and as these change constantly it’s important to review them on a regular basis with your adviser.

Cars And Tax

From 1 July 2017, new car threshold amounts apply for tax purposes.

Income Tax

There is an upper cost limit on the amount you use to work out the depreciation for the business use of your car. The car limit for the 2017-2018 financial year is $57,581 (unchanged from the prior year). For cars that cost more than this limit, the first year’s depreciation is calculated based on a cost of $57,581, and depreciation for the following years is then calculated on the written down value.

Goods and Services Tax (GST)

If you purchase a car and the price is more than the car limit, the maximum amount of GST you can claim is one-eleventh of the car limit amount i.e. $57,581/11 = $5,234. You can’t claim a GST credit for any luxury car tax when you purchase a luxury car, regardless of how much you use the car in carrying on your business.

Luxury Car Tax

From 1 July 2017 the luxury car tax threshold for luxury cars increased to $65,094. The threshold for fuel efficient luxury cars for the 2017-2018 financial year remains at $75,526. For more information on how to claim your car for work or business, check out our Tax Guide To Motor Vehicles.

ATO Small Business Benchmarks – How Do You Compare?

The ATO release small business benchmarks for a range of industries, and a range of business sizes. While the main purpose of the benchmarks for the ATO is to compare outlying business performance for tax avoidance, the benchmarks also provide an opportunity to compare your business to competitors of the same turnover size.

The ATO’s benchmark methodology has been verified as statistically valid by an independent organisation and is consistent with international approaches.

The benchmarks:

- are based on the biggest data set available – calculated from tax returns and activity statements from over 1.4 million small businesses

- account for businesses with different turnover ranges (up to $15 million) across more than 100 industries

- are published as a range to recognise the variations that occur between businesses due to factors such as location and businesses circumstances.

With the information that is available in the benchmarks, you can review what areas of your business might need improving in order to improve performance. If you are already performing better than the benchmarks, the comparison may also show you where you have a competitive advantage. You can access the small business benchmarks on the ATO website, or contact us to organise a review of your business against a number of benchmarks and performance indicators to find new ways to improve your performance.

Upcoming Dates

14 August 2017

Last day for lodgement of PAYG Payment Summaries with ATO where no tax agent involved in preparing the report

21 August 2017

Lodgement and payment of monthly July 2017 activity statements

25 August 2017

Lodgement and payment of quarterly June 2017 Business Activity Statement when lodged electronically through a tax agent

28 August 2017

Lodge Taxable Payments Annual Report for businesses in the building and construction industry

21 September 2017

Lodgement and payment of monthly August 2017 activity statements

30 September 2017

Lodge PAYG withholding payment summary annual report if prepared by a tax agent